Transfer Agency and It's Role in Digital, Tokenized and Fractionalized Securities

History of transfer agents and how blockchain can help provide a relatively more efficient process for the clearance & settlement of digital and tokenized securities

The National Clearance and Settlement System

The US securities market is one of the most liquid and critical capital market infrastructure in the US domestic and world economy, all of which is served by the U.S. clearance and settlement system (also known as ‘National C&S System’), which enhances safe, efficient and accurate settlement transactions between counterparties and financial intermediaries. The stakeholders in the clearance and settlement system includes settlement/transaction clearance, custodial and safeguarding, back-office and transfer agent counterparties, all of which is critical for the transparency and accountability of the securities market.

Investment securities confer certain intangible rights, such as the right to receive dividends, represent legal ownership in a company, partake in corporate governance and ability to transfer to other individuals and/or entities.

Bear with me as I try my best to explain the history of securities and clearance settlement system, the technology and structural enhancement (i.e. certified securities and uncertified securities/book-entry shares) the regulators had made over the decades to improve the process and finally, how the application of application technology can help further enhancement the settlement and clearance timeframe (T+5 to T+3 and hopefully, in the future T+1 and T+ near 0 settlement time) which ultimately helps brings more fluidity, efficiencies and minimize time arbitrage opportunities in the capital market.

The Uniform Commercial Code (UCC) and UCC “Protected Purchaser”

Generally, the transfer of securities is covered upon the Uniform Commercial Code (UCC), which is a set of regulatory framework that governs commercial transactions in the country, and it’s worth noting that UCC is not a federal regulation, but rather it’s an uniformly adopted state regulation by all 50 states (for the nuance with some slight variations state by state).

Under the UCC, ‘‘voluntary transfer of possession’’ is all that is required to conduct a transfer but in order to qualify as a ‘‘UCC protected purchaser’’, and therefore the purchaser can acquire the security free of any adverse claim, the purchaser must give value, not have notice of any adverse claim to the security from the seller and seller side counterparties before conducting the transaction transfer.

Even for a direct, agreed-upon transaction transfer between the buyer and seller, a series of steps must be complied and follow-through including security certificate must be endorsed by a credentialed 3rd party, guaranteed signatories, recordkeeping of document transfers, destruction of old certificates and creation of new certificates. There is where the application of blockchain technology can help remove the layers of inefficiencies in this process.

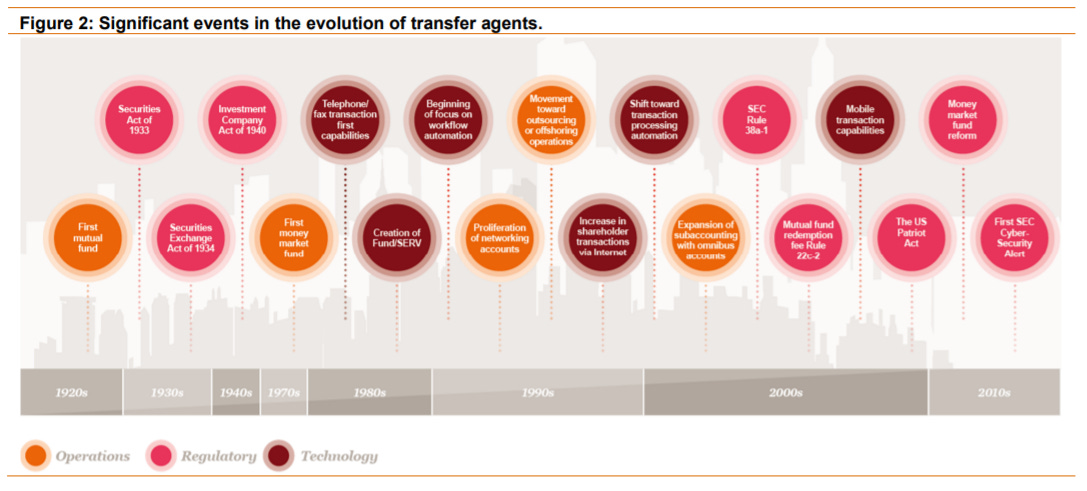

Transfer Agent

Transfer agents is arguably one of the most critical layer of this C&S System but it’s often times abstracted away from the general and professional public’s eyes. Transfer agents play a critical role in the securities settlement process, including functions such as:

Track, record, and maintain on behalf of issuers the official record of ownership of each issuer’s securities

Issue new security certificates

Cancel old security certificates

Transfer of those security certificates

Facilitate communications between issuers and registered securityholders

Make dividend, principal, interest, and other distributions to securityholders

Transfer Agent Processes for Transferring Certificated Securities

Security certificates are further broken down into two general categories, certified securities and uncertified securities or book-entry shares that in a sense acts as a mirrortable to the actual certified shares.

In order for a transfer agent to process the transfer of certified securities, the following series of manual steps must be complied:

A ‘‘ticket’’ pinned to the bundle of actual, physical documents that served as a transmittal letter and receipt of certified securities which includes the custodian’s instructions telling the transfer agent what action to take;, the security certificates of the selling securityholder, a power of attorney, a guarantee attorney or certificate, guaranteeing the genuineness of the signature of the selling securityholder indorsing the certificate over for transfer.

Upon receival of the ‘ticket’ the transfer agent would then perform a visual reconciliation to confirm that the number of securities shown on the ticket matched the number on the certificates, and if upon further audit discover an error, the ticket will then be return to the broker dealer in a process known as ‘window rejection.’

Further manual audit by the transfer audit will be conducted across all the documents submitted from the ‘ticket’ and if deficiencies are found, they would attach a rejection sheet to the certificate and return it back to broker in a process also known as ‘examination rejection.’

Finally, if the rest of the certificates were found to be in good order, the transfer agent would perform ‘‘stop checking,’’ the process of verifying each certificate number against a file maintained listing certificates reported stolen, missing, or with ‘stop transfers’ or legal holds.

Today, the ‘stop checking’ functionality performed by the transfer agent is audited against a national system operated by the Securities Information Center (‘‘SIC’’) as the US SEC’s designee for maintaining a database concerning missing, lost, counterfeit, and stolen securities that ‘‘reporting institutions’’ (brokers, dealers, registered transfer agents, certain types of banks, and others) report information to and inquire into concerning the status of securities certificates.

Tangentially, it’s equally as important for tokenized security records (application of blockchain and distributed ledger technologies) to be registered and maintained on the Securities Information Center (SIC) and/or the federal-level and SEC designee credential like database in order to minimize counterfeit and/or lost securities (arguably BC and DLT helps drastically minimize the risks aforementioned).

Paperwork Crisis of the 1960s and Uncertificated/Book Entry Securities

In 1977, the concept of the ‘uncertificated security’ was introduced in Article 8 of the UCC. Uncertified securities is a security that is not represented by a certificate.

The US Securities and Exchange Commission (SEC) started to regulate and further reinforce capabilities and requirements of the transfer agent layer with the advent of the adoption and application of technology in the US securities market in the 1970s. This change large reflects the multi-decade long evolution from a manual securities settlement process to a relative more automated electronic book-entry securities, functionally, similar to the Balaji’s Mirrortable concept.

Electronic book-entry securities means that the investor does not receive an actual, physical certificate (investor are entitled to physical certificate if requested) but instead, a custodian, usually a broker or transfer agent, maintains electronic records showing that the investor owns the particular security.

Electronic book-entry securities/uncertificated securities was prompted by Paperwork Crisis of the 1960s in which trading volume grew exponentially and exchanges had to close for a few days every once in a while during that decade to allow brokers and transfer agents to review, reconcile, authenticate and settle the certified securities. This created a cascading effect on the lost of investor confidence in the system, which prompted regulators, broker dealers, exchange operators and other stakeholders in the securities clearing and settlement process to work together to come up with a more efficient system so the first step of solution is the introducing of the Central Certificate Service (1968) by New York Stock Exchange (NYSE).

NYSE’s Central Certificate Service (1968) and DTC and Circle’s Verite

The NYSE establishment of the Central Certificate Service (‘‘CCS’’) as a division of the Stock Clearing Corporation allowed members of the NYSE to deposit their certificated securities with CCS, which would hold the certificates in custody and transfer them into the name of a CCS nominee. The certificated securities deposited by that member would be represented by an appropriate book-entry credit reflected in that member’s account at CCS. Because all securities held by CCS were registered in its nominee’s name, deliveries of securities between CCS members could be effected by appropriate credits and debits to the members’ securities accounts rather than by physical delivery of certificates. In this manner members’ accounts would be debited and credited to reflect transactions among them, but the registered owner of the securities—CCS’s nominee—would never change.

This is analogous to Zelle that was formulated based on the system of trust between banks inside the consortium and Circle’s most recently launched (Feb 2022) decentralized identity (KYC/KYB/AML/Accreditation) management API framework for participants in that consortium.

Unlocking Decentralized Identity with Verite

Over the next few years, CCS opened up to other exchange operators, and in 1973 CCS changed its name to the Depository Trust Company (‘‘DTC’’) and in late 1990’s, DTC merged with National Securities Clearing Corporation (NSCC) to form Depository Trust & Clearing Corporation, also known as DTCC, arguably one of the largest clearing and settlement house in the global securities market, which process, reconcile, clear and settles quadrillion amount of securities every single year. Below provides you a sense of their revenue stream, with settlement and clearing being the two largest drivers.

The Paperwork Crisis of the 1960s inspired the regulators and stakeholders to act and build a federal clearing and settlement system based on paperless movement of securities and in conjunction with the advent of technologies led the Congress to enact the Securities Act Amendments of 1975 (‘‘1975 Amendments’’) which sets the foundational blocks for a national market system and the National C&S System as they exist today.

In essence, the Congress directed the SEC to:

Facilitate the establishment of a national system for the prompt and accurate clearance and settlement of transactions in securities

End the physical movement of securities certificates in connection with the settlement among brokers and dealers of transactions in securities

Establish a system for reporting missing, lost, counterfeit, and stolen securities

Over the next few decades, technologies continues to get tested, experimented and evolved in the maturity of the clearing and settlement process of securities on a national level.

DTC’s Fast Automated Securities Transfer (‘‘FAST’’) Program

DTC introduce Fast Automated Securities Transfer, also known as FAST, in 1975, and got approved by the SEC in 1976. Prior to the introduction of FAST, transferring securities to and from DTC requires a few extra, redundant processes. For example for securities being deposited with DTC, participants would send certificates to DTC, which would then send the certificates to the transfer agent for reregistration into the name of DTC’s partnership nominee, Cede & Co., before returning the reregistered certificates to DTC, and in reverse, for securities being withdrawn.

“The FAST Program substantially reduced the movement of paper certificates by permitting transfer agents to become custodians for balance certificates registered in the name of Cede & Co. The balance certificate represents on the transfer agent’s books the sum total of shares for that issue held by all of DTC’s participants”

The FAST Program in essence not only reduced the # of steps need to settle and clear a security transaction, but it also removes or at least, brings transparency to the securities market by minimizing duplicate and/or fraudulent securities transactions because the balance certificate represents the total shares issued and held by all of DTC’s participants.

Further technological changes were made in subsequently decades to make it easier for institutional to do block transactions of securities rather than trade-for-trade and furthermore, with the introduction of The Direct Registration System (DRS) in 1996 further allows registered uncertificated (Balaji’s mirrortable concept) securities to be held directly on the books of the issuer’s transfer agent.

“Through DTC’s DRS Service, assets can be electronically transferred to and from the transfer agent and broker/dealer to easily move shares in and out of DRS”

Delivery-versus-payment privileges

In the early 1980’s, key exchange operators (in today’s digital asset world the equivalent of alternative trading systems ATS) introduced the concept of delivery-versus-payment, which in essence means payments are to be made prior to or simultaneously with delivery of the securities, which is logistically only possible with digital uncertificated/book entry security recognition.

By the late 1990s, DTC had become the largest depository in the United States and NSCC was the largest clearing agency, and subsequently, the SEC requested the M&A of these two entities in the 1999, which form the basis of The Depository Trust & Clearing Corporation (DTCC) that we know today.

Type of Security Ownerships

There are in essence two types of security ownerships, and this could impact how traditional and digital transfer agents set up their data structure and database:

Registered Securities Holder (RSH): RSH are treated as the registered person owner who are entitled to vote, receive notifications, and otherwise exercise all the rights and powers of an owner. RSH are listed directly on the records of the issuer or the issuer’s transfer agent under their own names. All communication between the transfer agents and issuers are to be direct to the RSH themselves. Registered owners can hold their securities either in certificated form or in uncertificated (i.e., book entry) form, such as uncertificated securities held through DRS.

Beneficial Owners (BO): Beneficial owners do not own the securities directly but generally have purchased them through an intermediary, such as a broker or a bank, and the owner’s name is bundled up in street name (could be name of the account type, name of broker/bank) through a book-entry account with that intermediary. The key differentiator here is that the intermediary, and not the transfer agent, is responsible for facilitate the responsibilities of a TA.

The intermediaries in the beneficial ownership scenario in essence provides a ‘sub-transfer agent service’ to the 'beneficial owners’.

This brings into the data structure managed under an omnibus system, one in which intermediaries maintain and keep records for individual shareholder accounts almost exclusively on their own books, aggregating records into a single account on the transfer agent system. This lowers the relative # of aggregated accounts that are passed through/look-through to the transfer agent for trade settlement.

Clearing and Settlement Process

Clearing of a trade in essence involved reconciling the terms set forth in the agreements by both the seller and buyer side of the transaction. This often times involve checking the identity of the buyer and seller (where KYC/KYB/AML/Accreditation credentials comes into play), the identity and quantity of the securities being traded, and the price, date, and other material details of the trade.

There are two major ways to clear a trade, bilaterally between two parties and central 3rd party clearance. The Black Monday of 1987 drove the majority of clearance today to be on the central 3rd party clearance route because that economic fallout caused a substantial amount of submitted, but unable-to-clear (or rather unwillingness-to-clear) scenarios.

Settlement is the transaction of their respective obligations for the trade, usually as defined as exchanging funds/capital for the securities.

Equities are often times settled in T+3, or 3 business days after trade date. Delivery today is highly probable be completed via a book-entry versus by exchange of physical certificates (reference the book entry, uncertificated process portion above). The settlement is done via DTCC and their Cede & Co. which facilitates book entry transactions involving electronic debits (on the seller’s side) and credits (on the buyer’s side) to the brokers’ securities accounts at the depository.

Furthermore, on the cash side of the trade, all money owed to or from a particular DTC participant will be netted down each day, so if the broker participant bought 1,000 shares of XYZ Company and sold 400 shares of the same XYZ Company, the broker’s DTCC’s account will be debited 600 shares of XYZ Company, which results in greater fluidity on the participant level so they do not have to keep double entry amount of capital needed since the daily reconciliation is on a net basis. This function could be uniquely challenging for T+0 or even T+1 settlement, at least from a participant liquidity perspective.

Most brokers today are part of the National Securities Clearing Corporation (NSCC) which is part of the DTCC, and these brokers are also known as clearing brokers, the order execution gets routed to national securities exchange. Whereas in scenarios where the broker is not part of the NSCC, also known as introducing broker or corresponding broker, the order execution will be re-routed to clearing brokers, who in turn will route it to national securities exchange.

I drew up a quick chart below to illustrate the contractual, clearing and settlement (securities via DTCC and cash via Federal Reserve Bank of DTCC).

Digital Transfer Agent and Tokenized Assets

Digital transfer agent also known as DTA (defined as one that utilized blockchain and DLT technology in fulfilling the transfer agency requirements) will play a continued critical role in the adoption of tokenized assets, especially tokenization of private assets, which is several magnitude bigger than the public market by valuation, and also happens to be one of the most illiquid and inefficient marketplace of security transaction. The DTA can govern both primary issuance and secondary issuances, each with it’s own implications.

Blockchain allows securities transactions and recordkeeping to be conducted and fulfilled without having another 3rd party intermediary (reference the bilateral trade process in the section above but it’s also worth noting on the prudency of having a 3rd party intermediary for clearing and settlement of securities (i.e. 1987 Black Monday occurred when bilateral trades, non-3rd party, was prominent, leading to many submitted-but-not-settled securities transactions).

Blockchain allows each piece of securities (direct on the registered securities holder RSH front and indirectly on beneficial owners BO front where each RSH will follow up to the BO level).

Each piece of security transaction can include the following to help streamline trust, limit the manual accuracy reconciliation necessary, minimize duplicates and fraud securities transaction:

CUSIP which provides a unique security and entity identifier that are recognized on the national exchange level

(Level 5)KYC/KYB/AML/accreditation credentials of both RSH and BO (roll up of individual RSH into BO) and credentials can be managed on a national level with the application of the necessary cryptographic and sharding protocols with substantial reduction in long-tail compliance cost for brokers.

Today, the ‘stop checking’ functionality performed by the transfer agent is audited against a national system operated by the Securities Information Center (‘‘SIC’’) as the US SEC’s designee for maintaining a database concerning missing, lost, counterfeit, and stolen securities that ‘‘reporting institutions’’ (brokers, dealers, registered transfer agents, certain types of banks, and others) report information to and inquire into concerning the status of securities certificates.

The national or consortium-like compliance credential management tool allows a more fluid clearing and settlement period, but it’s worth emphasizing the importance to ultimately give investors the controls on what, when, who and how often they want to share their credentials with the counterparties) based on settlement period.

(Level 4)Issuers and brokers can more easily comply their investors (both on RSH and BO basis) and compliance records with greater easy and transparency, especially in the status quo today where some compliance need (i.e. accreditation) is done via a manual process managed by independent, actively credentialed 3rd party.

(Level 1 and 4)Exact time and date stamp that cannot be tampered with, with records available on-chain for the public or at least, for the DTCC and the like--consortium to observe, which ultimately allowed for lower transaction fee and efficiency (analyses on time to clear and settlement between the different levels below) in term of time and transparency.

(Level 3)The routing between introducing broker —> clearing broker will be drastically minimize, so introducing broker will conduct the process and route the tokenized asset to clearing broker in seconds who will then submit to national exchanges for settlement.

(Level 5)Securities Exchange and Federal Reserve DTCC cash account is almost synonymous with alternative trading systems (ATS) and their processes but without all the clearing and settlement complexity below (or actually, there lack of).

(Level 5 and 6)Delivery-versus-payment privileges becomes more efficient so security transactions are released to the seller (cleared and settled) instantaneously as the cash are release to the seller. Cash be be fiat USD and/or CBDC.

(Layer 6)

Alternative Trading System ("ATS") List January 2022 SEC List

DTCC has an ALTERNATIVE INVESTMENT PRODUCT SERVICES structure that offers similar functionalities to the DTCC clearing and settlement traditional/non-alternative securities today.

But as we have observed in the past 70+ years of the DTCC (started with Paperwork Crisis of the 1960s, Securities Act Amendments of 1975, series of new regulations in subsequent years and decades, 1987 Black Monday inspired a more efficient clearing and settlement SOP, 1999 merger of DTC and NSCC to form modern-day DTCC, and introducing of DTCC alternative investment product services and more), we know more changes (hopefully more net positive, than net negative directionally), M&A and new regs will be introduced.

But it’s equally as prudent to recognize the adoption of this technology will come with the introduction of series of safeguards including coherent financial reporting structure, financial reporting cadence, audit requirements, management and corporate governance structure for private companies across different asset (equities, AR financing, money market, equity in companies, mortgage back securities etc.), (debt (corporate bond, treasuries, mezzanine debt etc.) and derivatives (options, commodities contracts, forex contracts etc.) classes.

Digital assets in the context of tokenized securities is here to stay as that is one of the more efficient ways to bring private assets (which is several magnitude larger than the public market by market cap/valuation) into the securities exchange, to help private assets get more liquidity (aka better price discovery and financing mechanism in conjunction to that), more securities and compliance visibility and transparency from the national/federal regulators perspective, and more.

Feel free to share your thoughts, reach out and more.

Epic breakdown!