Alternative Trading System (ATS) for Tokenized Assets, Royalty Rights, and Digital Rights

Alternative trading system, also known as ATS (some of which are referred to ‘dark pool’), is an SEC-regulated trading venue which serves as an alternative to trading at a public exchange (i.e. NYSE or NASDAQ). There are about ~50 active ATS’s in the US registered with the US Securities and Exchange Commission, and maintains an active, updated quarterly, list SEC Alternative Trading System ("ATS") List.

Regulation ATS (Reg ATS)

According to a SEC public opinion piece in 2013 titled “Alternative Trading Systems: Description of ATS Trading in National Market System Stocks” Trading on ATS’s currently consist of anywhere from 10-20% of the daily US equity trading volume but because of the opaque order matching reporting requirements of these systems today, it’s rather difficult to get a true accurate count, hence the wide range, but it further emphasizes the need to introduce a more robust operational and compliance framework.

Pre late 1990’s, the US equity exchange market was highly fragmented and with the advancement of technology, algorithmic trading, the DTCC’s introduction of The Direct Registration System also known as DRS (which was introduced in 1996 that further allows registered uncertificated (Balaji’s mirrortable concept) securities to be held directly on the books of the issuer’s transfer agent which prompted more efficient clearance and settlement of securities), prompted the introduction of Regulation ATS or Reg ATS in 1998 and officially adopted in 1999, drew a clearer definition of what is an ‘exchange’ and adopted further delineation of the compliance framework for ATS’s that are registered as a broker dealer (BD) or as a national exchange.

Ultimately, the introduction of further compliance framework for the ATS markets help facilitate a relatively fairer competition for market participants in the exchange market, at least in terms of trading volume (on the exchange participant level), though it’s worth emphasizing there are key institutional and structurally differences between an ATS and a traditional exchange. Although both exchanges and ATSs provide marketplaces for buyers and sellers to transact in securities, ATSs do not necessarily provide public information on the best prices available to traders within their system, which we will expand later in this piece.

Broker Dealer or National Exchange Registration

All Alternative Trading System (ATS) are subject to the regulations and guidance noted in Regulation ATS and must either:

Registered as a broker dealer (BD) license which is regulated by FINRA (you can search for any broker dealer here in FINRA BrokerCheck DB) or

Registered as a national exchange noted in 15 U.S. Code § 78f - National securities exchanges or

Operated by a national securities associations on in essence, a consortium or association of broker dealer as noted in 15 U.S. Code § 78o–3 - Registered securities associations

In addition, registered exchanges can become direct participants in the national market system NMS mechanisms, such as the ITS, Consolidated Tape Association (“CTA”), and the Consolidated Quotation System (“CQS”) which allows access to a wider liquidity market.

Further, only exchanges are eligible to be participants of the Options Clearing Corporation and thereby determine such matters as listing, registration, clearance, issuance and exercise of options contracts. ATS registered as a broker dealer cannot conduct options.

However ATS registered as an exchange would be required to comply with any SEC trading halt and circuit breaker rules during periods of market volatility and substantial market decline, which could present a structurally issue given the limited order volume on both side of the marketplace.

ATS Liquidity Provider and Market Depth

Regulation of ATS as broker dealers is the more common approach today and has work reasonably well to allow transparency, competition, and access. Furthermore, ATS allows currently illiquid asset to gain liquidity through these liquidity provider (LP).

This is a bit synonymous with the macro liquidity pool concept in DeFi, more specifically decentralized exchange DEX, given there is no 3rd party market makers involvement except the the market mechanism that naturally will push each LP to provide the best price to fulfill the order and minimize spread needs improvement (we will expand a bit more on NMS national market system for NASDAQ/NYSE that allows all the investor orders to be submitted on a national level and exchanges have the duty to find the more cost efficient exchanges to fulfill the orders, therefore, theoretically, making the price discovery and cost of transaction more efficient).

But ATS today is also not with its’s structurally challenges including that activity on some ATS' today is not fully disclosed to, or easily accessible by, public investors and may not have the adequate market manipulation and fraud surveillance or logic in place. Moreover, these ATS have limited obligation to provide investors a fair opportunity to participate in their market and/or to seek out the best transaction cost/spread for their investors.

This is a dichotomic contrast to the current public equities market structure which with the advent promulgation of Exchange Act Rule 11Ac1-4 requires the LP’s to display customer limit orders in market maker and specialist quotations, and also display of market maker and specialist price information contained in Electronic Communication Network (ECN), and NASDAQ’s linkage mechanism which showcase the best-priced orders for LPs to fulfill, thereby driving greater transparency and cost efficient in the market.

ECN is basically the price feed of all the orders received from liquidity providers - banks, brokers and private ECN traders . Liquidity providers are in competition among themselves for getting more trading orders. Liquidity providers are motivated to quote better in order to get higher trading volume. ECN helps drive National Market System (NMS)framework mentioned in this section above.

The ECN model allows to quote BID and ASK prices from different providers. As a result, ECN trading spreads are tighter than what any liquidity provider can propose individually.

At present, ATS are not fully integrated into the national market system NMS, leaving gaps of inefficiencies in market access and fairness, systems capacity, transparency, and surveillance but below are a general compliance framework as proposed by the SEC in the early-mid 90’s.

ATS General Compliance Framework

Capacity, Integrity and Security Standards

Establish reasonable current and future trading capacity estimates

Conduct periodic capacity stress tests of critical systems from the protocol, code review (Immunefi), database (AWS/Azure), DB infastructure (Hashicorp) security (Cloudflare) and more.

Develop and implement reasonable procedures to monitor system development and testing methodology and ensure an active log of these monitor reports are recorded.

Review the vulnerability of its systems and data center computer operations to internal and external threats, physical hazards, and others, and develop contingency plans.

Conduct an annual independent review of the systems that support order entry, order handling, execution, order routing, transaction reporting and trade comparison.

*If external auditors are used, ensure compliance with the standards of the American Institute of Certified Public Accountants and the EDPAA (electronic data auditor)

Recordkeeping and form ATS-R

Keep records (trading records, article of incorporation, partnership agreement etc) for at least 3 years, within the first 2 years in an easily accessible location

Form ATS-R requires transaction reports to be filed within 30 calendar days of the end of each calendar quarter, Form ATS-R requires the ATS to report the

Specifically, proposed Form ATS-R would require alternative trading systems to report on the following on a daily basis:Order Execution Information and Investor Compliance

Securities for which transactions have been executed

Number of trades

Number of shares traded

Total settlement value in terms of U.S. dollars; and

Price at which the order was executed

Size of the order executed (expressed in number of shares or units or principal amount); and

Time-sequenced records of order information

Compliance Identity of the parties to the transaction

All Order InformationDate and time (expressed in terms of hours, minutes, and seconds) that the order was received

Identity of the security (UUID, CUSIP and other identifiers)

The number of shares/units transacted on both side

The designation of the order as a buy or sell order

The designation of the order as a short sale order, if applicable

The designation of the order as a market order, limit order, stop order, stop limit order, or other type or order, if applicable

Order Expiration, Modification, CancellationThe date on which the order expires and, if the time in force is less than one day, the time when the order expires, if applicable

Any instructions to modify or cancel the order

The type of account, i.e., retail, wholesale, employee, proprietary, or any other type of account designated by the alternative trading system, for which the order is submitted

Safeguard Confidential Treatment of Trading Information

Delineation of access to investor confidential information and their orders to mitigate insider trading and protect investor confidential data.

Procedures to ensure that all its employees are unable to use any confidential information for proprietary or customer trading.

Procedures exist to ensure that employees of the alternative trading system cannot use such information for trading in their own accounts.

*These methods include physical separation, written procedures, separate personnel, and restricted access.

Prominent Alternative Trading System (ATS)

Some of the more prominent ATS players in the SEC Alternative Trading System ("ATS") List for non tradition securities or alternative investments including private startup equities, tokenized assets, royalty rights and digital rights are (in no particular order):

NPM Securities (NASDAQ Private Market arm that helps facilitate liquidity for private companies securities)

LEX (LEX Markets helps with tokenized of commercial RE assets and facilitate the trading of these tokenized RE assets via Nasdaq Marketplace Services Platform)

LEX’s corporate structure to hold these tokenized assets and securities is unique and I will attempt to expand more on it below.CartaX (block sales of employee and startup equities)

Figure ATS (crypto-based and blockchain-based mortgage securitization and lending)

Forge Markets (went public recently and does block sales of secondary transactions of employee startup equities)

IBKR ATS (Interactive Broker is one of the largest electronic trading platforms, and IBKR ATS is designed to trade both US and non-US equities, not alternative assets)

INXS (INX is one of the pure crypto and tokenized asset trading platforms)

PPEX (North Capital operates PPEX which is an ATS that’s heavily focuses on private asset/tokenized asset)

OPM (Oasis Pro Markets, LLC operates OPM ATS which is an ATS that’s heavily focused on private asset/tokenized asset)

Securitize Markets ATS (does primary and secondary transactions of private companies and tokenized/fractionalized assets)

RealCADRE LLC (CADRE, the fintech commercial RE startup, operates REALCADRE LLC. CADRE is a CRE investment that investors can either invest on a per deal basis or in a fund)

SeedInvest/StartupEngine (both top primary markets/fundraising lead gen for private companies recently set up an ATS to facilitate secondary markets)

tZero ATS (operated by tZero, which is majority owned by publicly traded Overstock, they have relatively more tokenized assets trading on the platform that most above)

ZX (Zanbato is the platform that facilitate private securities trade between institutional and family offices)

LEX Markets Corporate Structure

vs. Roofstock, Fundrise, CADRE, Figure

Lex Markets (personally a huge fan of the company!) is an investment platform that allows both accredited and non-accredited investors to buy equity security shares of pre-qualified commercial real estate, with quarterly distribution and ability to transact and get liquidity of your investment without lockups and holding period on their LEX ATS.

LEX ATS is build on top of Nasdaq Marketplace Services Platform, which provides a robust, and battle-tested technology and compliance layer for their ATS. According to the platform, all offerings on the platform are qualified through SEC Regulation A and Regulation A+ framework which enables non-accredited investors to participate on the LEX platform as well.

A few key differentiators observed on their platforms:

Distribution happens on a quarterly basis (not guaranteed) and there is a ex-distribution date similar to public equity dividend framework. Ex-distribution date is typically 10-14 days after the declaration of the dividend and record date is the date in which an agent of the issuer identifies all the current share or token holders, and therefore eligible for cash distribution.

Figuring our the dividend or royalty distribution model on (1) how often the distribution must happen, whether it be on a calendar Monthly, Quarterly, Semi-Annual basis or x # of regular or working day basis and/or other time structure will be key and (2) the agent record and calculation of distribution are both critical.LEX Offerings are structured as publicly traded partnerships (PTP) Only a portion of the cash distributed is deemed ordinary income, and investor may not owe taxes on the rest of the cash you received until they sell your shares on the secondary market, including on an ATS. Investor will receive a Schedule K-1 at the beginning of each year detailing what portion of the cash you received in the prior year was ordinary income. Volume on the secondary market on their limited offering is still low today.

IRS Definition of PTP

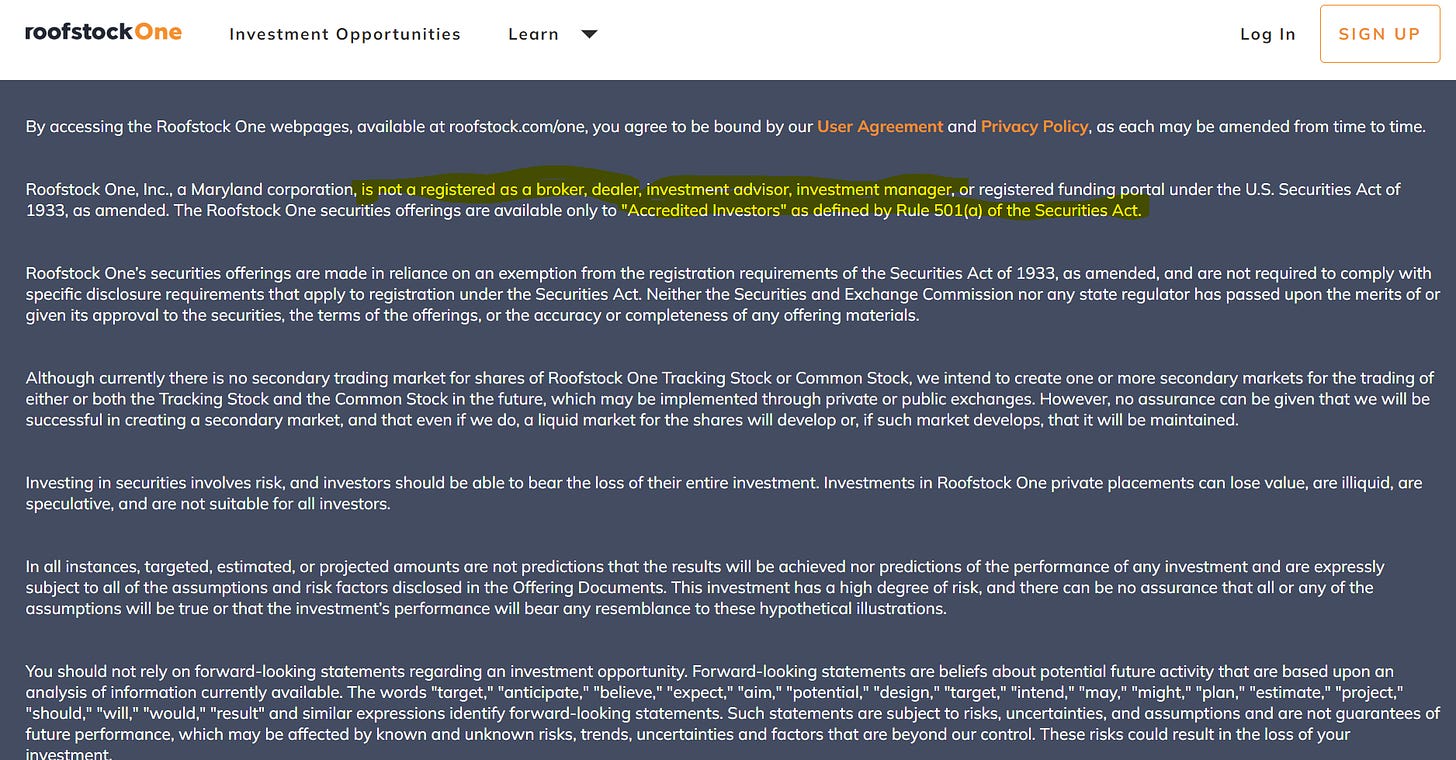

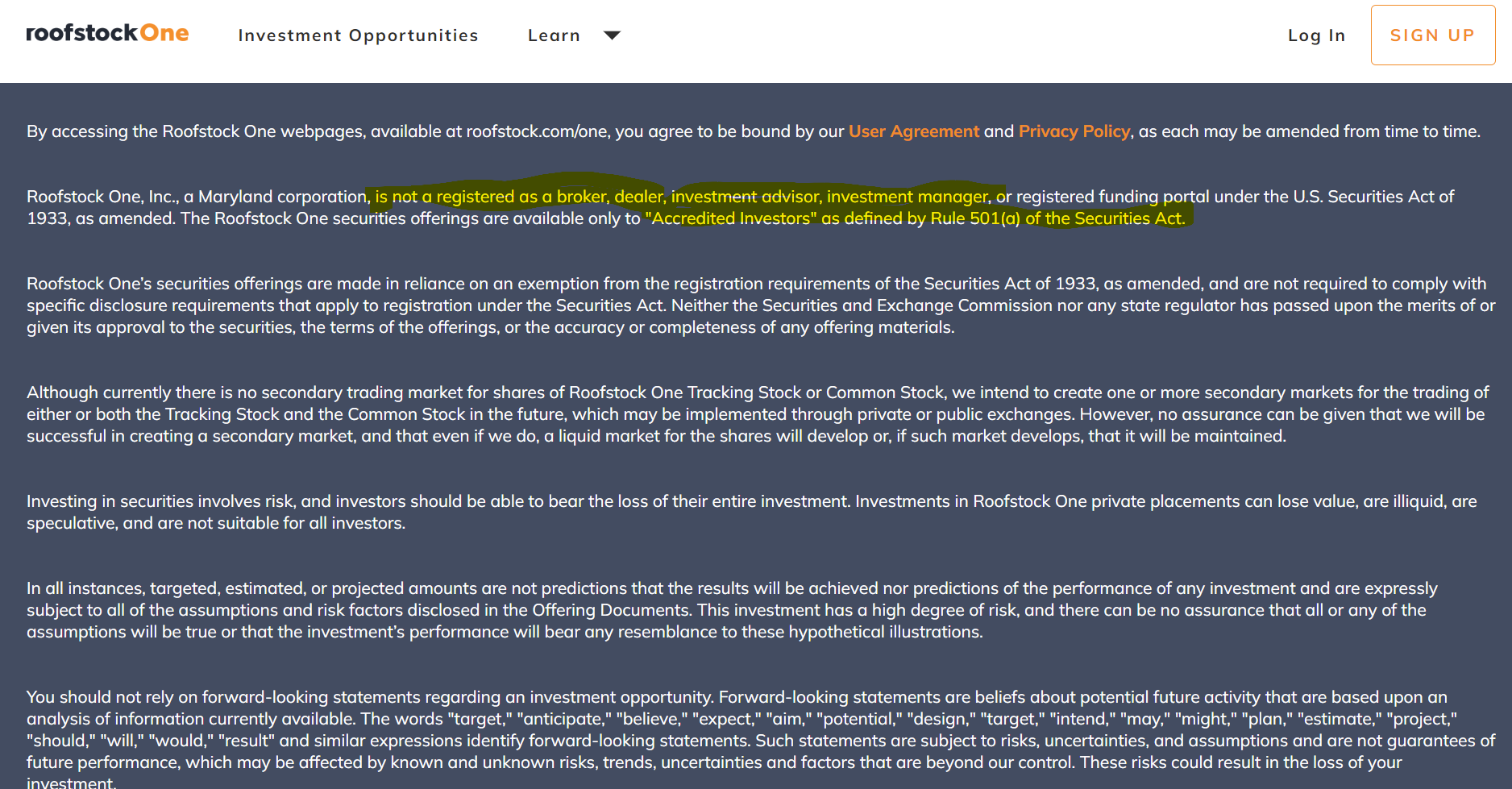

”A PTP is any partnership an interest in which is regularly traded on an established securities market or is readily tradable on a secondary market, regardless of the number of its partners. These rules do not apply to a PTP treated as a corporation under section 7704 of the Internal Revenue Code.”Roofstock One offers something similar to LEX Market, except as of today, the platform is geared towards accredited investors with a possibility of creating a secondary market for these token ownership.

CADRE on the other hand is doing Regulation A Offerings, which is similar to LEX except CADRE has an LLC attached to a portfolio of building whereas LEX as a Publicly-traded Partnership attached to a single building.

Figure ATS is another interesting participant in this space and they have one of the robust, public processes out there. Here is Figures secondary market (ATS) trading instruction.

Below are some unique takeaways from the list here including an ATS that requires somewhat of a manual confirmation via order submission interest on the buyers end and seller will have 24 hours to confirm the price in order for the trade to take place. Furthermore, the counterparty risk mentioned below is worth pointing out given the mechanism of how a trade is being conducted on Figure ATS.

Per SEC/FINRA requirements, participation in this ATS requires trade confirmation by both parties involved. The buyer and seller will have 24 hours to confirm a matched trade. Failure to confirm within the 24 hours will void the trade and prevent you from trading again. The SMS opt-in will allow the ATS to promptly notify you of a matched order. In addition, you will receive an email notification with a link to return to the ATS to complete your transaction.When you enter an order into the Figure ATS, you are contractually obligated to affirm and settle the trade if that order is matched on the Figure ATS. In the event you fail to perform your obligations to affirm and settle a matched trade, the counterparty to the trade shall have legal recourse against you, and Figure Securities will restrict your future access to the Figure ATS.

Tokenized real estate (SFR and CRE alike) and ATS that caters primarily to creating a secondary marketplace for this type assets is structurally synonymous with royalty and digital rights token (though it’s worth emphasizing there are a few different types of royalty rights out there each with its own caveat mainly surrounding which parties have legal claims to the one-time and ongoing royalty distribution and more) that have a ongoing dividend/distribution component to it.

Future of ATS

Current market developments and technological opportunities present both a series of opportunities and challenges for builders/operators, investors and regulators alike. On one hand, multiple and diverse markets can be facilitated on the Reg ATS framework thereby opening up investors to diverse asset allocation opportunities and meet their diverse trading needs and demands, while also allowing more liquidity into currently illiquid assets (which long tail allows more efficient price discovery), and on the other hand, warrants the need for a more robust, transparent and efficient regulation and reporting framework in order to provide clarity and trust to both the builders/operators and investors alike.